Pricing your bid correctly (or not) directly affects two key areas of your business: (1) either you win or lose the bid, and (2) either you gain profit or lose the contract. Is there anything more relevant than pricing in the preparation of the proposal? Definitely not. So how do you make the right price?

Pricing to Win.

Firstly, when it comes to pricing to win, you have to collect pricing information. The aim is to anticipate what government customers expect to pay. Check what suppliers are likely to offer as their rates for the product or service. You’re aiming for a choice between too low (which raises red flags with buyers) and too high (a quality you don’t have a chance of winning).

When gathering pricing information, you concentrate on “same” or “similar.” You want to look at the same or related products or services, companies, customers, end-users, etc. We want to look at relatively recent arrangements, too.

The method is roughly analogous to that of a lawyer gathering case law to support his legal arguments; or explaining to his client how the court will decide the conflict. We are looking for similar trends of evidence in cases handed down by the competent courts of the particular jurisdiction. When he can’t find anything comparable, search beyond that jurisdiction in other cases. He begins nearby, seeing what he can do, and if possible spreads from there.

Here’s What you Should Follow:

Start with current customers and end-users in pricing contracts. Have they recently purchased the same or related products or services? A couple of years ago? How about the others in the Agency? Was it within the department? In short, start to close and expand as needed.

Unlike the commercial sector, government agencies generally have to disclose what they have paid for the same product or service in the past. Note, too: customers are more willing to talk if you see them before the contract is written. Upon release, the questions to buyers must be replied in writing and sent to the other bidders.

The Internet is another source of the pricing information; For example, the Defense Logistics Agency releases the National Stock Number (NSN) statistics on price history on the Internet. The DLA pricing history shows previous sales of the NSN object and the price paid for each purchase.

Similar information can be displayed at local and state buying pages. Data on the costs of suppliers can also be accessed by visiting government e-marketplaces based on multiple contract schedules. The prices of the product and service inventory are publicly available in these markets; but note that the offers displayed may be better than the rates that the alternative would have provided for public procurement.

Pricing to Profit.

First, when it comes to pricing to make a profit, you have to take a hard look at your own expected costs of delivering under the deal. When calculating costs, a company new to the federal contract will consider using a Certified Public Accountant (CPA). Furthermore the experienced in the federal contract is calculated and they hire the experienced members.

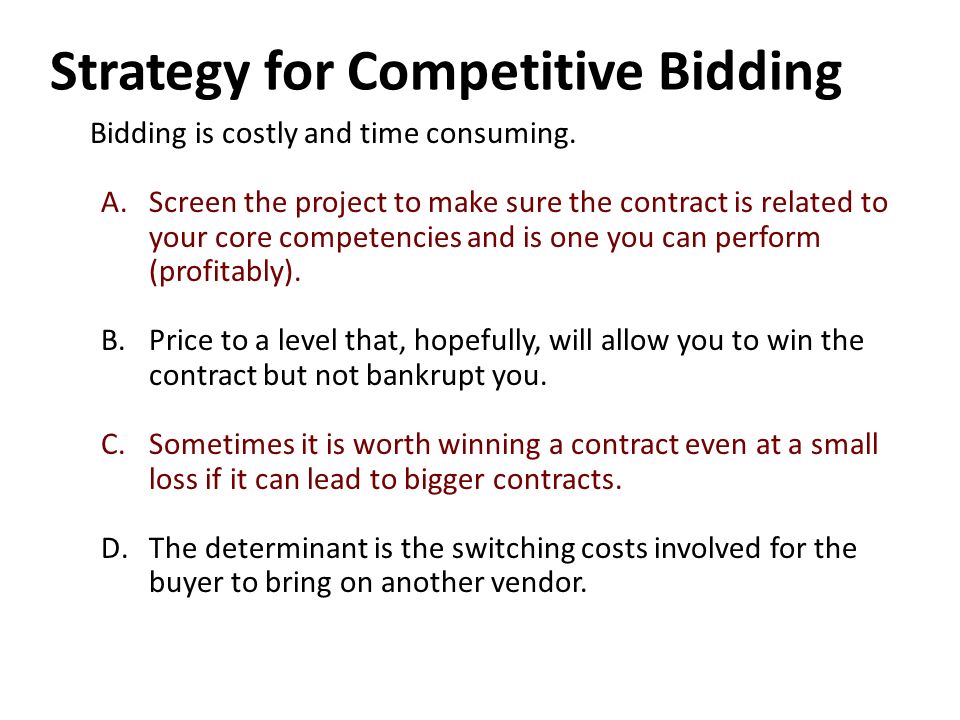

If a bid price that falls within the spectrum of what is required (based on your intelligence gathering) leaves the business without benefit, then there is possibly only one decision to be reached: do not submit a bid. (Some companies are willing to experience a business failure hoping to make it up for others—”foot in the door “principle. For most businesses, this is a risky strategy.)

IFBs and RFQs pricing.

For fixed price bidding, losing a competitive bid is not as bad as winning an unprofitable bid because most products are often bought, and the expense of bid planning is relatively low. It is a valid strategy to continue with higher prices on initial tenders for regularly purchased items. Since the winning price is public information, you can use that information to set lower prices for future bids.

Determining the bid price is the single most crucial aspect of winning fixed bids because the price is the main (and, in many cases, the only) factor in determining the winner, assuming that the bidder is responsive and responsible.

Do not submit a bid until you know precisely what you are going to deliver and that you can make a reasonable profit at the bid price. Ambiguities and complexities usually give rise to issues. Pay particular attention to the terms and conditions of contract, distribution and payment of bids. In deciding the price of the bid, be sure to include all inventory, labour, payroll, shipping and transport costs.

Pricing Negotiated Procurements.

In the planning of a contract estimate for a negotiated offer, bidders will apply their maximum cost and demand. Keep in mind, however, that the negotiated procurement process is more versatile than the sealed contract procedure: there is a better opportunity to seek changes to the terms, conditions of agreement or supply and payment. Note, too, that consumers should rely on a total cost analysis. Therefore, be prepared to support the bottom-line dollar figure with facts and figures.

Although RFPs usually involve some negotiation, they do not occur in all instances. The contracting officer may approve a request without any discussion, so, again, close attention to detail is essential. Don’t get trapped at a price that’s too big.

The bidding methods for contracts vary considerably depending on the type of product or service provided in the sense of the deal. An agreed price is usually set in four stages.

- Build a work plan.

- Estimate direct labor and other direct costs using the work plan.

- Build indirect costs at an indirect expense point.

- Determine any charge or benefit.

Developing a work plan and direct costs are the administrative tasks that line managers and technical staff create. Collectively, this party will decide how to execute the contract at the lowest possible cost best.

The creation of indirect costs is typically the responsibility of the financial department of the company with the assistance of CPA if appropriate.

Proposed model price.

To put all this in perspective, it is helpful to see a model price proposal. We’ve put one on the web for your convenience. The concept design is for a fictional research and development organization. This shows the main facets of cost and price growth, including the estimation of several indirect costs.

Estimate of indirect costs.

Indirect costs shall include all expenses which can not be directly attributed to a project, company or contract. These include items such as fringe benefits, overhead and general and administrative expenses. Costs found to be unallowable by the federal government must be subtracted from gross indirect costs in the measurement of indirect costs. Such variable expense levels are then added to direct costs in the calculation of total costs. The model price implementation provides an example of indirect expense rate estimates.

Factors that influence indirect costs.

On the surface, the definition of indirect cost-rate estimates shown in the model price proposal seems to be straightforward. In fact, the issue of indirect costs and their effect on bidding at the lowest possible cost can be very complicated. The foregoing are just a few issues relating to indirect costs:

- Would different types of labour be divided into separate divisions to reduce payroll and fringe benefits?

- Which types of labour are subject to margin profit scales?

- Should you use independent contractors or temporary workers to reduce costs, and is this allowed under federal regulations?

- What is the effect of seniority on labour costs?

- How can the cost of fringe benefits and the productivity of workers be held down at the same time?

This blog was written by Linda Rawson, who is the founder of DynaGrace Enterprises (dynagrace.com) and the inventor of WeatherEgg (weatheregg.com). She, along with her daughter, Jennifer Remund make up the mother-daughter duo of 2BizChicks (2Bizchicks.com). For further information, please connect with Linda on LinkedIn, or contact her at (800) 676-0058 ext 101.

Please reach out to us at GovCon-Biz should you have any questions.